Fraud detection

Understanding the data

df = pd.read_csv('creditcard.csv')

df.head()

| Time | Amount | class | v1 | v28 |

|---|---|---|---|---|

| 1.0 | 149.62 | 0 | -1.359807 | -0.021053 |

- NOTE There are 28 ‘v’ features : v1,…,v28

- Due to privacy reasons most colums dont have a column name

- Time : not enough information about this feature, going to remove

- amount : the monentary amount of the transaction that was flagged as fraud

- classes :

- 0: No fraud

- 1: Fraud

Exploratory Analysis (EDA)

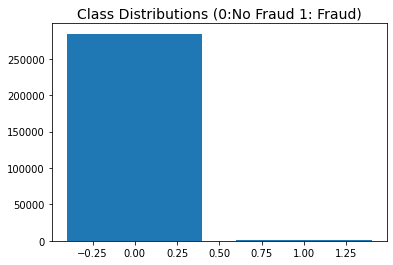

plt.bar(x=[0,1],height=[df['Class'].value_counts()[0],df['Class'].value_counts()[1]])

plt.title('Class Distributions (0:No Fraud 1: Fraud)', fontsize=14)

| Class | |

|---|---|

| 0 | 284315 |

| 1 | 492 |

amount_val = df['Amount'].values

fig,ax = plt.subplots()

sns.distplot(amount_val, color='r',ax=ax)

ax.set(title='Distribution of Transaction Amount')

ax.set_xlim([min(amount_val), max(amount_val)])

plt.show()

- Tansactions are mainly of smaller amounts

Metric Selection

- very imbalanced class distribution, positive class is minority

- positive class more important than negative class, need to detect if fraud occurs with high confidence

- e.g. 90% precision

- False negatives; falsely classifiying fraud sample as not fraud is very costly need to minimise.

- need as low as possible

- trade-off: high recall as possible due to False negatives

- but precision needs to be above a threshold to be useful

- Precision, recall,f1 measure and False negatives going to be used to compare models via cv

Pre-processing

- Dataset was scaled, used robust scaler which is more robust to outliers

- To better visualise the data and conduct multi-vartiate analysis, will implement a random under sampling technique, which undersamples the majority class, creating a more balanced dataset

rob_scaler = RobustScaler()

X = df.drop(['Class','Time'],axis=1)

y = df['Class']

X_scaled = rob_scaler.fit_transform(X)

X_scaled_df = pd.DataFrame(X_scaled, columns = X.columns)

rus = RandomUnderSampler(random_state=42)

X, y = rus.fit_resample(X, y)

sns.countplot(y)

balanced_df = pd.DataFrame(X.join(y))

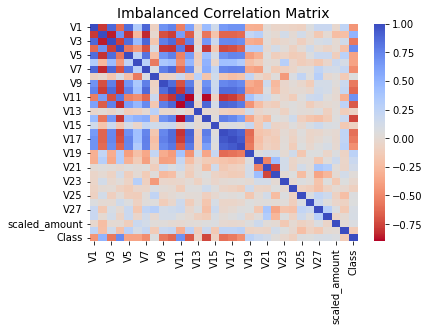

corr = balanced_df.corr()

sns.heatmap(corr, cmap='coolwarm_r', annot_kws={'size':20}).set_title("Imbalanced Correlation Matrix", fontsize=14)

- v4, v11 features are highly positively correlated with class

- v14 andv10 are highly negatively skewed with class

- no features are hightly correlated with eachother

- if there was highly correlated features , should remove

Model selection

- Needed to split the data into training and test sets, then apply transformation in pipeline

- to prevent leakage when estimating model preformance on via cross-validation.

- Used stratified random sampling, as dataset very imbalanced

- reloaded orginal unbalanced dataset

X = df.drop(['Class','Time'],axis=1)

y= df['Class']

X_train, X_test, y_train, y_test = train_test_split(X,y,stratify=y,random_state=1)

Baseline score, without resampling or specialised imbalanced algorithms

- First going to use:

- naive model: dummy classifier which outputs uniform results

- logistic regression

- random forest

- neural network

- Aim: get a baseline score without specialised algorithms designed for imbalanced learning

- naive algorithms without resampling etc

- The first 3 models were implemented using the sci-kitlearn library

- stratified 10 fold cv was used to calculate f1, precision and recall values

- The neural network model was implemented using the tensorflow library

sci-kit learn (model 1,2 and 3)

from sklearn.dummy import DummyClassifier

from sklearn.pipeline import Pipeline

pipe1 = Pipeline([

('scaler',RobustScaler()),

('model',DummyClassifier(strategy='uniform'))

])

pipe2 = Pipeline([

('scaler',RobustScaler()),

('model',LogisticRegression())

])

pipe3 = Pipeline([

('scaler',RobustScaler()),

('model',RandomForestClassifier())

])

from sklearn.model_selection import cross_validate

from sklearn.model_selection import StratifiedKFold

cv = StratifiedKFold(n_splits=10)

scores= ['f1','precision','recall']

navie_cv_results = cross_validate(pipe1,X=X_train,y=y_train,cv=cv,scoring=scores,n_jobs=-1)

logistic_cv_results = cross_validate(pipe2,X=X_train,y=y_train,cv=cv,scoring=scores,n_jobs=-1)

randomForest_cv_results = cross_validate(pipe3,X=X_train,y=y_train,cv=cv,scoring=scores,n_jobs=-1)

The mean f1, precision and recall scores

model_1: naive algo

| 0 | |

|---|---|

| test_f1 | 0.00347783 |

| test_precision | 0.00174494 |

| test_recall | 0.503979 |

model_2: logistic regression

| 0 | |

|---|---|

| test_f1 | 0.685409 |

| test_precision | 0.852982 |

| test_recall | 0.577477 |

model_3: random forest

| 0 | |

|---|---|

| test_f1 | 0.840989 |

| test_precision | 0.948857 |

| test_recall | 0.756156 |

- clearly the naive algo performs the worst

- mean scores from cv does not show the whole picture

- must visualise learning curves to diagnose any problems in the learning stage

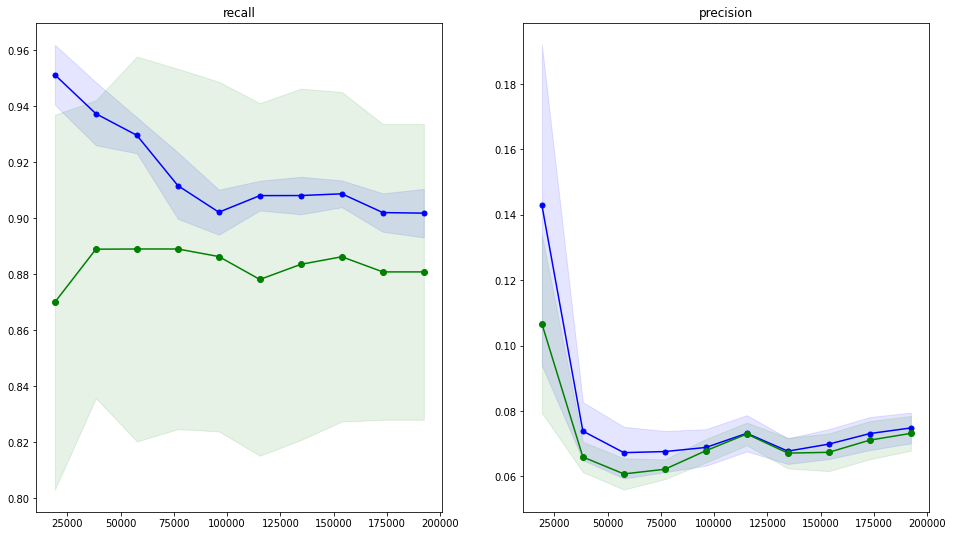

The precision and recall learning curves

model_2: logistic regression

_algo_learning_curve.png)

- logistic regression seems to be the best, but recall score is low

model_3: random forest

_learning_curves.png)

- randomforest is overfitting

- represented by large gap between the training and test scores

Tensorflow neural network

- The neural network will be built via a different library called keras

METRICS = [

keras.metrics.Precision

keras.metrics.FalseNegatives

keras.metrics.Recall

]

def make_model(metrics=METRICS, output_bias=None):

if output_bias is not None:

output_bias = tf.keras.initializers.Constant(output_bias)

model = keras.Sequential([

keras.layers.Dense(

16, activation='relu',

input_shape=(train_features.shape[-1],)),

keras.layers.Dropout(0.5),

keras.layers.Dense(1, activation='sigmoid',

bias_initializer=output_bias),

])

model.compile(

optimizer=keras.optimizers.Adam(learning_rate=1e-3),

loss=keras.losses.BinaryCrossentropy(),

metrics=metrics)

return model

model.compile(

optimizer=keras.optimizers.Adam(learning_rate=1e-3),

loss=keras.losses.BinaryCrossentropy(),

metrics=metrics)

return model

EPOCHS = 100

BATCH_SIZE = 2048

early_stopping = tf.keras.callbacks.EarlyStopping(

monitor='val_prc',

verbose=1,

patience=10,

mode='max',

restore_best_weights=True)

model = make_model()

model.summary()

| type | Output Shape | Param |

|---|---|---|

| Dense | (None, 16) | 480 |

| Dropout | (None, 16) | 0 |

| Dense | (None, 1) | 17 |

- Total params: 497

- Trainable params: 497

- Non-trainable params: 0

_learning_curve.png)

concluding first stage

- logistic regression and Random Forest is shortlisted

- the complexity of the algorithms will be increased

Specialised algorithms

-

Implemented SMOTE and cost-sensitive learning on the shortlisted model

-

logic of using cv for imbalanced learning:

- up/down sampling done in inside cv

- imblearn.pipeline extends scikit-learn pipeline.

- Up/downsampled only the data in the training section

- Fit the model on the up/down sampled training data

- Score the model on the (non-up/downsampled) validation data

recall/precision trade-off

- SMOTE and balanced class wieghts increases recall at the cost of precision

from imblearn.pipeline import Pipeline as imbpipeline

pipeline1 = imbpipeline([

['smote', SMOTE(random_state=11)],

['scaler',RobustScaler()],

['classifier', LogisticRegression(random_state=11,penalty='l2', n_jobs=-1, max_iter=1000)]

])

- precision of ~0.03 is not acceptable